Page 29 - Energize September 2021 HR

P. 29

VIEWS AND OPINION

The economics of grid defection revisited

What seemed like a novelty is becoming commonplace

by Fereidoon Sioshansi, PhD, Menlo Energy Economics

n 2014, the Rocky Mountain Institute (RMI) published a report titled The economics of grid

defection in which it showed how different regions of the US could experience grid defection as the

Icost of self-generation – primarily from rooftop solar PVs – would fall below retail electricity rates.

It was a prophetic report – scary if you were a regulated utility with high retail tariffs in a sunny

region of the US such as Hawaii or California. The report, as with many others from the RMI and

others, was, however slightly ahead of its time. For example, while it saw the combination of solar plus

batteries as a major threat, it did not foresee how quickly the costs of both technologies would fall.

The report posed the question: “What happens when solar and batteries join forces? Together

they can make the electric grid optional for many customers – without compromising reliability

and increasingly at prices cheaper than utility retail electricity.”

Adding, somewhat optimistically, “Though many utilities rightly see the impending arrival

of solar-plus-battery grid parity as a threat, they could also see such systems as an opportunity

to add value to the grid and their business models. The important next question is how utilities

might adjust their existing business models or adopt new business models – either within existing

regulatory frameworks or under an evolved regulatory landscape – to tap into and maximise

new sources of value that build the best electricity system of the future at lowest cost to serve Fereidoon Sioshansi

customers and society.”

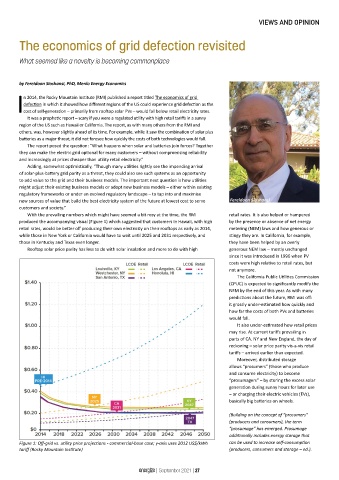

With the prevailing numbers which might have seemed a bit rosy at the time, the RMI retail rates. It is also helped or hampered

produced the accompanying visual (Figure 1) which suggested that customers in Hawaii, with high by the presence or absence of net energy

retail rates, would be better off producing their own electricity on their rooftops as early as 2014, metering (NEM) laws and how generous or

while those in New York or California would have to wait until 2025 and 2031 respectively, and stingy they are. In California, for example,

those in Kentucky and Texas even longer. they have been helped by an overly

Rooftop solar price parity has less to do with solar insolation and more to do with high generous NEM law – mostly unchanged

since it was introduced in 1996 when PV

costs were high relative to retail rates, but

not anymore.

The California Public Utilities Commission

(CPUC) is expected to significantly modify the

NEM by the end of this year. As with many

predictions about the future, RMI was off:

it grossly under-estimated how quickly and

how far the costs of both PVs and batteries

would fall.

It also under-estimated how retail prices

may rise. At current tariffs prevailing in

parts of CA, NY and New England, the day of

reckoning – solar price parity vis-a-vis retail

tariffs – arrived earlier than expected.

Moreover, distributed storage

allows “prosumers” (those who produce

and consume electricity) to become

“prosumagers” – by storing the excess solar

generation during sunny hours for later use

– or charging their electric vehicles (EVs),

basically big batteries on wheels.

(Building on the concept of “prosumers”

(producers and consumers), the term

“prosumage” has emerged. Prosumage

additionally includes energy storage that

Figure 1: Off-grid vs. utility price projections - commercial-base case; y-axis uses 2012 US$/kWh can be used to increase self-consumption

tariff (Rocky Mountain Institute) (producers, consumers and storage – ed.).

energize | September 2021 | 27